College costs can be daunting, yet saving is one strategy that could make it easier to reach future goals. Beyond parent income and savings, other family members can contribute and enjoy tax benefits while helping loved ones reach their potential. During this holiday season, consider the gift of education, more meaningful and lasting than any store-bought item.

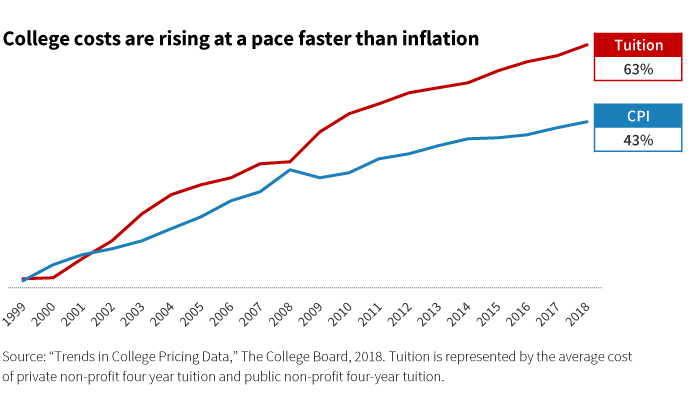

The importance of college savings is clearer now more than ever before. Increased saving means less borrowing for students. Student debt in the United States reached a record $1.5 trillion this year. For the 2017–2018 academic year, the average student college debt totaled $29,000 (The College Board).

Using a 529 college savings plans allows assets to grow tax free. Account owners pay no federal income taxes on earnings while the account is invested and no federal income tax when the money is withdrawn to pay for qualified college expenses.

There are several advantages to saving with a 529 plan that makes gifting easier and offers tax advantages.

- Gift with strings. Parents can remove assets out of their estate for tax purposes while remaining owners of the account and retaining control of the assets. This also applies to other family members, including, but not limited to, grandparents, aunts, and uncles.

- Front-load gifts. A special gift tax exclusion allows donors to give five years’ worth of gifts in one lump sum to a single beneficiary in a single year, without triggering a gift tax. The earlier a 529 plan is funded, the more time the assets have for potential growth and the benefits of compounding interest.

- “Super-size” a contribution to a 529. If donors act before year-end, they can front-load six years’ worth of gifts within a short time frame. Consider giving $15,000 (maximum annual gift allowance) in December, and then an additional $75,000 in January. The end result is funding $90,000 at roughly the same time. A married couple could double this amount.

Additional benefits of a 529 plan

The ability to change beneficiaries is another benefit to a 529 plan. If the child does not attend college, the account beneficiary may be switched to another family member. Account owners can change the beneficiary to another family member as many times as they want. Unlike custodial accounts, such as UGMA or UTMA, the assets do not shift to the child at the age of majority.

Proceeds from a 529 can be used at any accredited college to pay for tuition, fees, room and board, books, and other qualified expenses. In addition, up to $10,000 per student per year may be used to pay tuition at any public, private, or religious elementary or secondary school.

It’s never too early to start

Assets in a 529 are allowed to grow tax free, and the account can benefit from compounding over time. For more information about getting started, read Putnam’s investor education piece “Early college planning for a growing family.” It is also important to consult with an advisor to set goals, understand how the investment works, and explore strategies for staying on track.

319773

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.