Health care is one of the leading concerns among individuals planning for retirement. With costs continuing to increase, and rising inflation weighing on purchasing power, planning for future health expenses is a key topic among individuals still in the workforce as well as those in retirement.

For those age 65 and older, Medicare forms the foundation of health coverage. Today, more than 60 million people are enrolled, and that total is expected to exceed 80 million in 25 years.

Medicare does not cover everything, and generally, supplemental coverage is needed. Many investors find it confusing to navigate the program. To understand the basics of how Medicare works, read Putnam’s investor education piece, "Three key things to understand about Medicare.”

Opportunity for change

Each year, Medicare holds an open enrollment period that allows participants to sign up or make changes to existing plans and supplemental coverage. Enrollment is available for individuals age 65 and older as well as people with disabilities.

According to the AARP, many enrollees overlook this opportunity to possibly save money and improve their coverage. The Kaiser Family Foundation notes that Medicare participants could save thousands of dollars by choosing a prescription drug or Medicare Advantage plan that best fits their needs.

This year, open enrollment runs from October 15, 2023, through December 7, 2023.

Here are possible changes for retirees to consider:

1. Switch to a different Medicare Part D plan

It is not uncommon for a Medicare Part D plan to change its list of covered drugs, which may lead to higher out-of-pocket expenses. Individuals on Medicare should closely monitor and analyze their “Plan Annual Notice of Change” document, which details any changes to costs and coverage for the upcoming year. The document is typically mailed by the end of September. Participants can also contact the provider directly. If the new drug formulary no longer covers essential prescriptions, enrollees may want to research other Part D plans that can address their needs. Medicare recently updated its plan comparison tool, “Medicare Plan Finder.”

2. Compare Medicare Advantage plans

Medicare Advantage plans are private plans that bundle together Medicare Parts A, B, and D, and typically offer additional benefits such as vision, dental, and hearing coverage. For 2023, the limit on annual out-of-pocket expenses is $8,300 for in-network services and $12,450 for in-network and out-of-network services combined.

Enrollment in Medicare Advantage plans has nearly doubled over the past decade, with many participants seeking the potential for lower premiums and out-of-pocket costs, and more comprehensive coverage. Today, more than 30 million people are enrolled in Medicare Advantage (KFF). This represents a little more than half of the eligible Medicare population. However, like Medicare Part D, the drug formularies that companies use may change from year to year. As a result, retirees should make sure important prescription drugs are still covered under the plan. In addition, because most Medicare Advantage plans are administered as health maintenance organizations (HMOs), plan participants should monitor any changes to their list of covered providers.

Lastly, those who have moved or are contemplating moving to a different state will need to determine if their current plan is available in their new home state. In addition, there may be plans available in your new home state that are better suited for your needs that were not available in your previous home state.

3. Change from Medicare Advantage to original Medicare (or vice versa)

While Medicare Advantage plans typically offer additional benefits not included with original Medicare, these services come with an important trade-off. Participants must receive services in network, or risk potentially high out-of-pocket expenses. Individuals who relocate, or anticipate the need to receive care from out-of-network providers, may place a higher premium on flexibility than cost. Retirees switching from Medicare Advantage to original Medicare will want to add a supplemental Medigap policy to avoid the possibility of significant out-of-pocket costs.

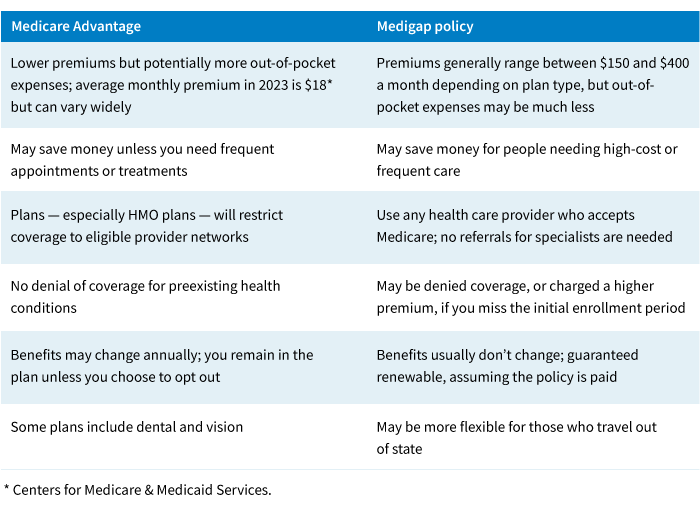

Here's a look at some of the differences in supplemental coverages — Medicare Advantage versus obtaining a Medigap policy.

Note: Enrolling in a Medigap policy after your six-month Medigap open enrollment period around your 65th birthday may result in higher premiums for those with preexisting medical conditions.

Health care is part of a comprehensive plan

Maintaining adequate health care coverage is an important part of a comprehensive retirement plan. Unexpected medical bills have the potential to drain savings that otherwise could have been used for traveling and philanthropy, as well as leaving behind a legacy of wealth for family members. Working with qualified professionals during the open enrollment period may help improve coverage and manage future health care costs.

335222

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.