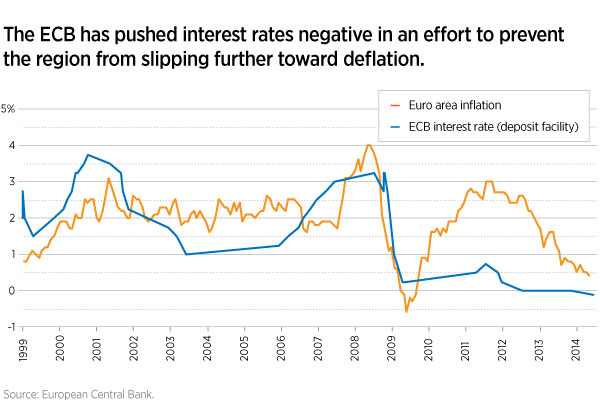

In early June, the European Central Bank embarked on what could be a series of policy decisions to stimulate the region’s economy and reduce the risk of deflation. The ECB cut its key refinancing rate to a historic low of 0.15% and took the unprecedented step of instituting a negative deposit rate of -0.10%, which would effectively charge banking institutions a fee to park money at the ECB. By making this move, the ECB hopes to encourage banks to lend more and thereby get more capital working in the economy, but it is an experimental measure that has yet to be tested on a large scale.

Refinancing operations may help banks in Europe’s periphery

A measure that we believe could potentially be quite helpful was the ECB’s implementation of targeted long-term refinancing operations (TLTROs), which are also designed to encourage lending and stimulate growth. In our view, ECB actions can have a meaningful impact on the share prices of banks as well as the markets in general. For equity portfolios with a pro-cyclical bias, this could translate into highly positive news.

The introduction of TLTROs will allow banks to borrow funds from the ECB for four years at a very low cost. This will be especially beneficial to peripheral European banks, which have typically had to borrow at much higher rates. This will enable the banks to lend money at relatively low rates to consumers and corporate entities and still make an attractive profit on the spread between those rates and their TLTRO funding cost. A number of European banks, particularly in Spain and Italy, performed well in the second quarter — both because of the TLTRO announcement and because government borrowing costs declined during the period, which had a positive effect on the banks.

Corporate demand for credit remains a question

At a recent financial-market conference in Madrid, many companies acknowledged that TLTROs could be quite helpful. But they also suggested there is a credit demand problem in the market — that is, too few corporations are confident enough in the economic recovery to borrow more at this stage. After all, just because the ECB has announced it is ready to hand out money at low cost doesn’t mean European corporations will start lining up to borrow. Again, the ECB is trying new measures to stimulate the economy. We consider these promising avenues but by no means a guaranteed cure. Nevertheless, if demand for credit picks up, then we think at some point TLTRO funding could become extremely attractive to lending institutions.

Read Putnam’s Q3 2014 Equity Outlook on Slideshare or download the complete pdf at putnam.com.

289942

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.