Planning for health care in retirement can seem like preparing for the unpredictable. Outside of preventative and chronic care, the need for long-term care and supports can arise suddenly in later years. Medicare has limits on how much of long-term care is covered, and the out-of-pocket expenses can rise quickly.

Individuals just turning 65 today have a 70% chance of needing some type of long-term care services and supports, according to the Department of Health and Human Services. About 65% of people will need some care at home for an average of two years. In facilities, 35% will require an average of one year in a nursing home and 13% will use less than one year in assisted living.

In addition, about 20% of people will need long-term care for longer than five years.

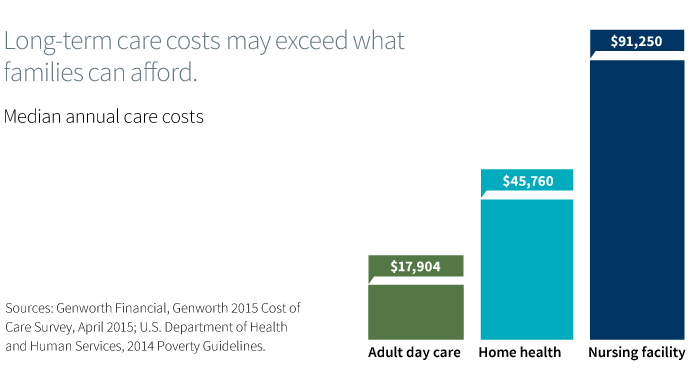

Annual long-term care costs can vary by state, from a high of $250,000 in Alaska to $60,000 in Oklahoma. The 2015 Genworth Cost of Care Survey identified 18 states where long-term care costs average more than $100,000 annually.

Nursing home care, among the most costly, does not always mean permanent residency. An increasing number of people use nursing homes for a short length of stay for rehabilitation. Among seniors, the average length of stay for a man is roughly 10 months and 1-1/2 years for a woman. While Medicare may cover a portion of short-term stay, the rest of the rehab can mean substantial costs to retirees.

The long-term care insurance decision

In addition to including health expenses in an overall financial plan, there are additional considerations including ways to pay for them. Insurance-related options, such as long-term care insurance, may help pay for these costs later in life. But the decision can be a complicated one, as investors grapple with the potential need for insurance, and the cost of premiums, which can be high.

Ultimately, health-care expenses in retirement are part of comprehensive financial planning. It can be helpful to discuss this important portion of the household budget with a financial advisor who understands your individual financial situation. For more information on planning for health care in retirement, see Putnam’s investor education article, “Successful retirement planning must consider health-care factors.”

300804

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.