The SECURE Act became law in December and introduced many changes to retirement accounts that will take effect in 2020. One significant change was the repeal of the stretch IRA strategy.

Popular with estate plans

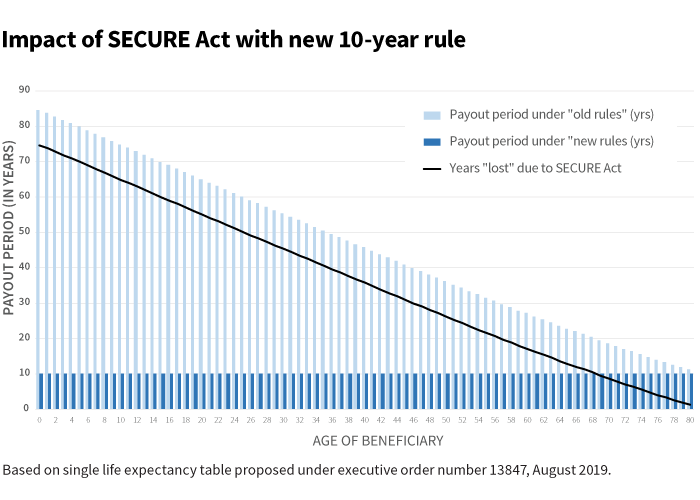

For roughly two decades, those inheriting individual retirement accounts (IRAs) had the choice to calculate required distributions based on their remaining life expectancy, referred to as the “stretch IRA” strategy.

This concept allowed the IRA to continue to grow tax deferred even after the death of the account owner. The younger the beneficiary meant the greater the remaining life expectancy, resulting in lower required distributions from the IRA. Of course, if they wished, beneficiaries could take more than the required minimum.

Repeal of the stretch under the SECURE Act

- Many beneficiaries are required to fully distribute inherited account balances by the end of the 10th year following the year the account owner dies. There is no requirement for annual distributions, the account just has to be fully liquidated by the end of the 10th year.

- This change applies to both inherited IRAs (both traditional and Roth) and defined contribution (DC) plan accounts for deaths occurring after 2019.

- If the account owner died prior to 2020, heirs can still generally stretch using life expectancy payments out of the IRA. However, this only applies until the death of the heir/beneficiary, at which point the new 10-year rule applies.

Exceptions apply

The SECURE Act created a new type of beneficiary known as the eligible designated beneficiary (EDB). These individuals may calculate required distributions based on remaining life expectancy.

There are five types of the EDB:

- Spouses

- Disabled (as defined under IRC §72(m)(7))

- Chronically ill

- Minor child of IRA owner, until the age of majority is reached at which time the 10-year rule applies

- Beneficiary not more than 10 years younger than the IRA owner

In general, conduit trusts for these beneficiaries that meet certain qualifications will be considered EDBs for purposes of using life expectancy payments.

Key challenges with the new 10-year rule

Bracket creep for heirs

Under the new law, most non-spouse heirs are required to distribute funds out of the retirement account by the end of the 10th year following the year the account owner dies. Note that there is no annual distribution requirement under this rule; the heir can distribute any amount as long as the account is fully liquidated over the required 10-year time frame. This can result in accelerating taxable income, creating “bracket creep” for heirs, some of whom may be in their peak earning years. Heirs need to consult with their tax advisor to determine a plan for tax-efficient distributions over the 10-year time frame.

Lack of control “beyond the grave”

- The repeal of the stretch provision directly contradicts one planning strategy: assigning a trust as the beneficiary of an IRA

- Prior to the SECURE Act, IRA owners who wished to control distributions to heirs following their death could choose to assign a trust as the beneficiary of the IRA. Following the death of the account owner, these trusts often limited payments to heirs to required minimum distributions only (based on the life expectancy of the heir)

- This can occur for a variety of reasons such as where there is concern of leaving a younger beneficiary too much wealth too quickly

- Often referred to as “look through” or “see through” trusts, these trusts had to meet certain requirements to ensure required distributions could be stretched based on the remaining life expectancy of the trust beneficiary

- With the repeal of the stretch provision, a full distribution of the account in many cases (unless an exception applies) will be required within the 10-year time frame.

Seek advice

Estate plans that incorporate the stretch IRA strategy need to be revisited. Investors should consult with their financial advisor or estate planning expert to explore alternative strategies.

320262

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.