- The Fed’s facilities have increased liquidity and confidence in the markets and, in turn, stabilized financial assets.

- Volatility spiked in June amid a surge in COVID-19 cases, but risk appetite was positive during the month.

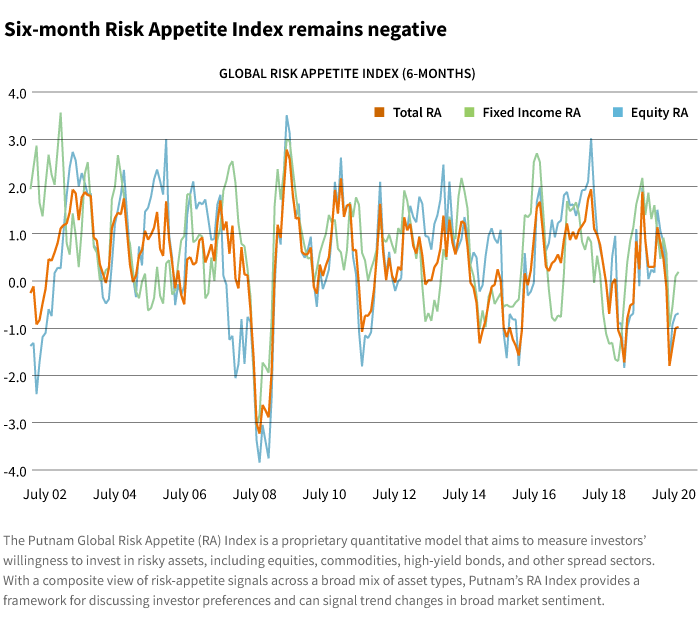

- The six-month risk appetite remains negative, and long-term Treasury bonds are the best performers during this period.

June was a volatile month for risk appetite. Early in the month, the risk rally was accelerating, and the U.S. dollar was depreciating against other currencies. The dispersion in returns, adjusted for volatility, was disappearing and optimism was rising as the global economy was reopening. Higher asset returns and the outperformance of sectors that were hardly hit by the coronavirus pandemic were probably incompatible with a world still dealing with the virus and recovering only with plenty of policy support.

Fed slows pace of bond buying and global rates rise

But as states eased mobility restrictions, there was a spike in COVID-19 cases in a large number of places such as Florida and Texas. The reopening and rising number of cases had been going on for a while, but asset markets didn’t seem to care very much about it until concerns about insufficient Fed policy materialized. The main sell-off started just after the Fed meeting in mid-June and continued for a few days. A key factor is the Fed’s rapid tapering. During the heat of the crisis, the Fed was buying $75 billion of Treasury securities a day. As the Treasury market stabilized and financial markets started to recover, the Fed reduced the pace of purchases week by week down to $4 billion per day.

In the first two months of this tapering, Treasury bond rates managed to stay in a very narrow range despite the Fed’s reductions. In late May and in June, as the Fed continued to taper, global rates started to rise. Since this coincided with rising optimism over global growth, there was a case to be made that the Fed’s tapering was in line with the economic developments.However, we need to remember that the risk rally since late March was due to the proactive policy response.

Without a proactive Fed, the risk rally would be in trouble.

Without a proactive Fed, the risk rally would be in trouble. The Fed clearly got nervous about the sell-off and quickly announced its intentions to purchase individual corporate bonds. A real rate rally followed and stabilized risky asset markets. As the economy enters the second half of the year, we believe the Fed will need to step in with more policy support as the initial phase of growth fades. Whether that will be through more explicit yield-curve control or an expansion of its quantitative easing program isn’t yet clear.

Investor sentiment remains fragile

Although risk assets gave back some of the earlier gains, they managed to end June in positive territory. Since the markets peaked early in June, secular winners outperformed. However, for the whole month, the laggards in the recovery periods remained outperformers. Non-U.S. assets and currencies, in addition to energy commodities, were notable outperformers.

The three-month Risk Appetite Index, which shows the historic returns of the second quarter, and the six-month Risk Appetite Index, which indicates year-to-date performance, point to the outperformance of sectors, countries, and currencies that benefit from or are less severely hit by the pandemic. The six-month risk measure, which covers the first half of 2020, remains negative. In addition, long-term Treasury bonds — anything longer than the 10-year — are the best performing assets during the first half of the year.

322601

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.