With student loan debt at all-time highs, and potential relief programs under debate by policymakers, the need for families to save is more important than ever.

While student loan forgiveness is a leading topic among lawmakers, the future of these proposals is unclear. Between Congress and the administration there is no agreement on how much relief to provide. In addition, a moratorium on student loan payments introduced during the pandemic has already been extended once. Currently, the administration is considering whether to move the deadline out further.

With no relief in the near term, student debt, however, continues to grow.

Student debt totaled $1.7 trillion in 2021, and most of that debt (92%) involved federal student loans. The remaining portion comprises loans from private providers.

Most graduates (65%) have some student loan debt. Individual borrowers hold an average of $30,000 in debt for a bachelor’s degree, and more than double that amount, around $70,000, for a master’s degree. (Education Data Initiative).

Trends in aid, cost

| Federal aid | Of total federal financial aid, loans comprise 65% Federal financial aid has decreased 36% over the last 10 years |

| College cost | Average private four-year college = $55,800 Public, in-state = $27,330 |

Source: College Board, Trends in college pricing 2021.

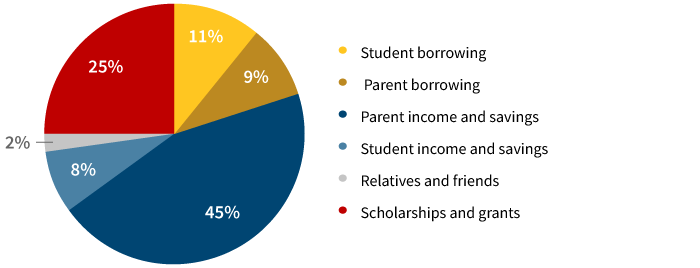

Income and saving play a big role in paying for college

Parents’ income and saving play a major role in paying for college. According to Sallie Mae, parents’ contributions make up 45% of the funds needed for college. Scholarships and grants represent 25%, and student borrowing (11%) and parent borrowing (9%) are also top sources.

Source: Sallie Mae, 2021.

Saving can be challenging. In 2021, 37% of families used a 529 college savings plan. These plans offer certain tax advantages. Account owners pay no federal income taxes on account earnings while the account is invested. There is also no federal income taxes when the money is withdrawn to pay for qualified college expenses. In certain cases, contributions to the account can be removed from the owner's estate for tax purposes, yet they can retain control over the assets.

With borrowing part of the equation for most families, there are many options for student loans, either from the federal loan programs or private lenders.

Student loan options

- Subsidized loans are need based, no interest accrues while student is in college, lower interest rate, and generally the best loans to use first

- Unsubsidized loans are available to all students regardless of financial need, but interest accrues immediately

- No co-signer required

- Typical amount available to borrow annually is generally $5,500 to $12,500 and is based on the FAFSA

- Origination fees exist (roughly 1% of amount borrowed)

- Additional options include federal Parent PLUS loans and loans available from private providers. However, these loans typically have less favorable terms

- For example, the current interest rate for a federal student loan for undergraduates is 3.73% with an origination fee of around 1%. Consider the current interest rate for a Parent PLUS loan is 6.28% with an approximate 4% origination fee (U.S. Department of Education, studentaid.org). While Parent PLUS loans are not based on financial need, applicants have to pass a credit check to qualify

Repayment options

For most student loans, payment starts 6 months after leaving school. If another option is not selected, the default is a 10-year repayment plan.

Another option is a graduated payment plan where loan payments start lower and gradually increase.

With an income-driven repayment plan payments are based on a percent of income. These loans are designed to be more affordable. If the borrower qualifies, the balance is forgiven after 20 to 25 years. However, the borrower may have to pay more interest over a longer term than they would with a standard repayment program over 10 years. There is also the potential that payments may not big enough to cover the interest that is accruing.

Under the Public Service Loan Forgiveness (PSLF) program, the borrower works for a non-profit or government agency and can qualify for a smaller monthly amount based on income, with the balance forgiven after 10 years. There may be other federal or state forgiveness programs for areas such as teaching and health care. Overall, since inception, a very small number of borrowers have participated and benefitted from the federal income-driven repayment plan or PSFL.

According to educationdata.org, less than 1% of borrowers will eventually benefit from student loan forgiveness, based on how the programs are currently structured.

Borrowers may also consider consolidation or refinancing.

For loan consolidation, the interest rate is based on a weighted average of outstanding loans. For individuals with a loan at a considerably higher interest rate, it may make sense to prioritize paying that one off and consolidating the rest. Borrowers may also be able to get a discounted interest rate (e.g., 0.25% on certain loans) if they set up auto payments out of a bank account.

Refinancing is offered by private loan companies, and may be able to lower the interest rate. However, this option is not reversible and the loan is no longer eligible for federal forgiveness plans.

Outlook for loan forgiveness proposals

Loan forgiveness has become challenging for different reasons. A large percentage of the population has not attended college and many taxpayers question why their tax dollars are being spent to bail out student loans. In addition, a blanket forgiveness would benefit many middle and higher-income professionals. According to the non-profit Committee for a Responsible Federal Budget, 73% of the benefits from cancelling $10,000 worth of student loan debt per individual would flow to the top half of income earners.

A moratorium on federal student loan payments has been in been in place since March of 2020 due to the pandemic. This has been extended several times and is set to expire at the end of August, it would not be surprising if another short-term extension of the moratorium was announced.

In the loan forgiveness debate, some Democratic senators, including Elizabeth Warren (MA) and Bernie Sanders (VT), support forgiving a large amount of student debt — $50,000. The Biden administration has floated a lower number — $10,000 — but has pushed back on Congress to address via legislation, given concerns on potential legal challenges if the administration takes direct action outside of Congress

Instead of blanket loan forgiveness based on a specific dollar amount, the Biden administration recently said they want to make it easier for lower-income student borrowers to get debt forgiveness through existing income-driven repayment plans. These plans were introduced during the 1990s, but the take-up rate has been low. The administration is also signaling they want to target any loan forgiveness to lower-income households.

While the moratorium for loan repayment may be extended, the future of federal loan forgiveness proposals is unclear.

Get advice, make a plan

It’s important for families to craft a plan and set goals. In 2021, more families than ever before (58%) had a plan to pay for all four years of college (Sallie Mae). A financial advisor can help create a plan and optimize strategies to meet those goals. Saving through a 529 plan is an important component and can help reduce the amount that may need to be borrowed.

329898

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.