We are now halfway through the year, and a leading question among financial advisors during my recent travels is the status on the 10-year rule for distributing inherited retirement accounts introduced by the SECURE Act. (Read our original post on the 10-year rule.)

Although the Treasury Department issued proposed regulations for the new 10-year rule in February 2022, heirs are still waiting for final clarification.

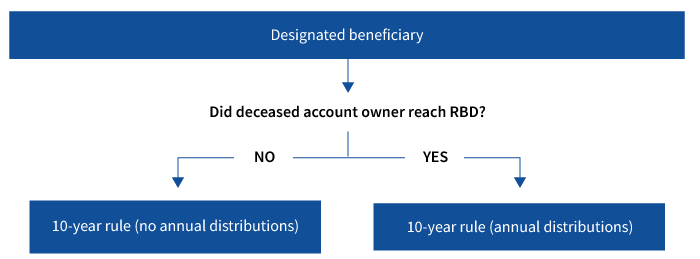

A central provision of the SECURE Act is the new 10-year rule, which impacts most non-spouse beneficiaries when inheriting an IRA or retirement account. The rule applies to distributions from inherited retirement accounts where the owner died after 2019. It may apply to successor beneficiaries where the original beneficiary died after 2019. The prevailing interpretation was that the rule provided flexibility for heirs to decide when to take distributions over a 10-year period. The only requirement was the inherited account had to be fully distributed by the end of the 10th year. Note that some beneficiaries, such as spouses, are not subject to the new 10-year distribution rule.*

But the industry received a surprise with February’s proposed regulations. Among them was further detail on how the 10-year rule would apply.

In short, if the deceased account owner had reached their required beginning date (RBD), then the beneficiary would have to (at least) take annual distributions based on their life expectancy for the first nine years, followed by a full distribution by the end of the 10th year. Of course, the beneficiary could always take the distribution sooner, but this was the minimum requirement. If the account owner died prior to RBD, then the 10-year rule — without the annual distribution requirement — would apply.

Sources: Based on proposed Treasury regulations subject to change. Setting Every Community Up for Retirement Enhancement Act of 2019; Treasury Department, Required Minimum Distributions, Notice of proposed rulemaking and notice of public hearing, REG–105954–20. Required beginning date is generally April 1 of the year following the calendar year in which the account owner reaches age 73. In the case of an account owner dying after RBD, designated beneficiaries and eligible designated beneficiaries may opt to base annual distributions on the remaining life expectancy of the deceased account owner.

Where do we stand right now?

We are still awaiting final word from the Treasury Department on when and if these proposed regulations — and their interpretation of how the 10-year rule should work — will be final. The proposed regulations could be modified as well. To address the question of whether heirs who inherited an account after 2019 should be taking annual distributions now, the IRS issued Notice 2022-53 last fall. The IRS effectively said that heirs subject to the 10-year rule where the owner died post-RBD did not have to take annual distributions for 2021 and 2022 while the Treasury regulations are still pending. Technically, the penalty for not taking RMDs in these cases is waived.

Should heirs take a minimum distribution for 2023?

While we await final word from the Treasury Department, there remains a lack of clarity on exactly how the 10-year rule applies. Heirs may be wondering if they should plan on taking a distribution for this year. Unless they need the funds to meet current expenses, there’s an opportunity to use the funds for a more advantageous purpose; or, if it is favorable from a tax perspective (for example, if they are in a lower tax bracket), heirs may want to wait until there is further clarity from the Treasury. We may expect these rules to be finalized before the end of 2023, but there is no guarantee. If there is no answer this year, we would expect the IRS to issue a similar notice stating that the penalty for not taking a distribution (in this case, for 2023) would be waived. It’s important for those inheriting a retirement account to consult with a financial professional to determine a distribution plan that makes sense for their particular situation.

*There are exceptions to the 10-year rule for certain account beneficiaries like spouses. These are referred to as “Eligible Designated Beneficiaries,” or EDBs, and are exempt from the 10-year rule. Instead, these heirs can generally calculate required annual distributions based on their remaining life expectancy, without being subject to the 10-year rule. For more information, read our piece “Distribution planning under the SECURE Act."

333979

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.