Health savings accounts, which provide tax-advantaged savings for qualified health expenses, have grown significantly in recent years. HSAs are available to individuals enrolled in high-deductible health plans. At the end of 2014, the Employee Benefit Research Institute found there were 2.9 million HSA accounts with a total of $5 billion in assets, and nearly 80% of those accounts were opened since 2011.

HSAs are also part of the health-insurance reform proposal being debated on Capitol Hill. The bill provides for expanded use of these accounts.

Contributions to HSAs are made with pretax dollars, and the funds grow tax free. There are limits to contributions, and individuals who are 55 and older may make an additional $1,000 catch-up contribution. Withdrawals are not taxed as long as they are used for qualified medical expenses. Since an HSA does not have a time limit for distribution, the funds can be used for health-care costs in retirement.

Funding an HSA through an IRA transfer

In addition, there is a strategy that investors may use to fund an HSA using an individual retirement account (IRA). But it may be used only once in a lifetime.

A Qualified HSA Funding Distribution allows investors to transfer funds from an IRA to an HSA tax free and penalty free (no 10% early withdrawal penalty). The amount transferred cannot total more than what the investor would be allowed to contribute to an HSA for that year. In 2017, the maximum amount is $7,750 for a 55-year-old with family health coverage who has not made other HSA contributions during the year.

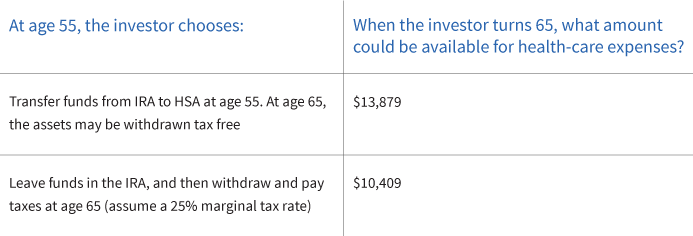

Investors may benefit

Consider a 55-year-old who can choose whether to transfer the maximum amount allowed — $7,750 — from an IRA to an HSA, or leave the money in the IRA. Assume that the individual plans to retire at age 65 and the account has a 6% growth rate.

More details on HSAs can be found on the Internal Revenue Service’s information page. It is important to discuss planning for health-care costs in retirement with a financial advisor. Since investors can only use this funding strategy one time, it is important to consider this transfer in the context of an overall financial plan.

306085

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.