The Federal Reserve is expected to raise short-term interest rates at least two more times in 2018. After three hikes in the past year, the Fed noted at its recent meeting that additional rate increases are possible.

With many financial plans tied to Internal Revenue Service (IRS) interest rates, there are several strategies that investors may want to consider before rates get much higher, and other strategies that become more attractive at higher interest rates.

Two key IRS interest rates that influence financial planning:

Applicable Federal Rate (AFR). The IRS publishes three interest rates each month: a short-term (under three years), mid-term (3 to 9 years), and long-term (over 9 years) rate, based on average market yields from securities of different maturities (U.S. Treasury bills). The AFR is used as a guideline for determining interest rates on private loans as well as for many other tax-related applications.

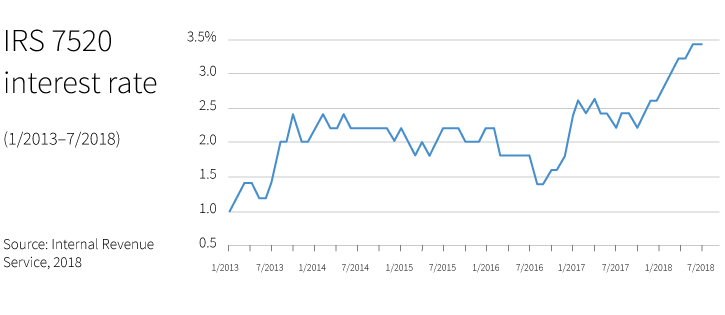

IRS section 7520 rate. Published monthly, this rate is equivalent to 120% of the federal AFR mid-term rate rounded to the nearest two-tenths of a percent. The rate is often referred to as the “discount” or “hurdle” rate for determining the value of certain property interests in split interest trusts, including charitable trusts and Grantor Retained Annuity Trusts (GRATs).

Planning considerations

Strategies to consider before interest rates increase further:

Intra-family loans or installment sale of a family business. These strategies can be effective in transferring wealth from one generation to the next. At lower required IRS interest rates, financing a family loan or a series of installment payments is less expensive.

Grantor retained annuity trust (GRAT). Allows the grantor to transfer wealth within a trust in exchange for an annuity payment for a fixed number of years. Over the trust term, growth in assets within the trust in excess of the required interest rate for the annuity payments (IRS Section 7520 rate) are effectively transferred to beneficiaries free of federal gift and estate tax.

Charitable Lead Trust (CLT). To the extent interest rates are low (IRS Section 7520 rate) and assets inside the trust appreciate, the remainder interest left to beneficiaries after the trust term will be higher.

Strategies to consider as interest rates increase:

Charitable Remainder Trust (CRT). A donor receives regular interest payments from the trust over a certain time frame. Any remaining interest within the trust after the term ends is transferred to the charitable organization. Higher interest rates will generally result in a higher charitable tax deduction for the donor when the trust is funded.

Qualified Personal Residence Trust (QPRT). This allows families to transfer a residence while enabling the owner to continue living there over the trust term. Higher interest rates will generally result in a lower taxable gift when the trust is established.

Consider an example of the impact of rising rates on a GRAT. Over the term of the trust, annuity payments are made from the trust back to the grantor, based on the value of the assets initially transferred to the trust, and the prevailing IRS interest rates. At the end of the term, if the assets have appreciated more than the IRS interest rate, the remaining value is transferred to beneficiaries, free of gifts and estate taxes.

In this example, consider a GRAT created with a term of three years and funded with $1 million.*

- Assume growth in assets over the 3 years is 10% annually

- Compare residual wealth inside the trust left to beneficiaries at IRS Section 7520 rates of 2%, 3%, and 4%

After the trust term ends, the amount of wealth transferred to the next generation will total:

2% = $182,244

3% = $160,815

4% = $138,248

As this example highlights, the higher the IRS interest rate, the lower the residual amount transferred to beneficiaries free of transfer taxes. In fact, an IRS 7520 rate of 2% will yield almost $45,000 more left to beneficiaries, compared with an interest rate of 4%.

Seek expert advice for advanced strategies

In considering any of these advanced strategies, it is important to work with a qualified estate and tax planning professional. While lower interest rates may present a window of opportunity, it is important to speak with an advisor before deciding to incorporate a trust or other strategy into a financial plan.

*Source: Putnam research

312254

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.