With the reduction in marginal income tax rates, the new tax law is lowering the cost for investors who decide to convert traditional IRA assets to a Roth IRA.

Although taxpayers may save money on this transaction under the Tax Cuts and Jobs Act, the law also eliminated the possibility of changing your mind. The process of reversing a Roth conversion — or recharacterization — was repealed under tax reform.

Recharacterization is eliminated

The new law eliminates the ability of taxpayers to recharacterize or undo a Roth IRA conversion. While conversions cannot be recharacterized, contributions can still be recharacterized.

In the past, IRA owners could fully or partially reverse a conversion before filing their taxes (generally within the tax filing deadline plus a six-month extension).

For example, if IRA owners converted a traditional IRA to a Roth IRA in January 2016, they would have until October 15, 2017, to reverse that decision.

Some taxpayers recharacterized the transaction if they decided the tax liability was too high or if it triggered other tax issues such as the taxation of Social Security benefits or the exposure to the 3.8% Medicare surtax on investment income. Others sought a “redo” if the Roth IRA declined in value. For example, if a taxpayer converted a $50,000 IRA that declined in value to $40,000, there would not be an advantage in realizing the $50,000 in income for an account that has lost value.

Without the ability to recharacterize, more thoughtful analysis is needed before completing a Roth IRA conversion.

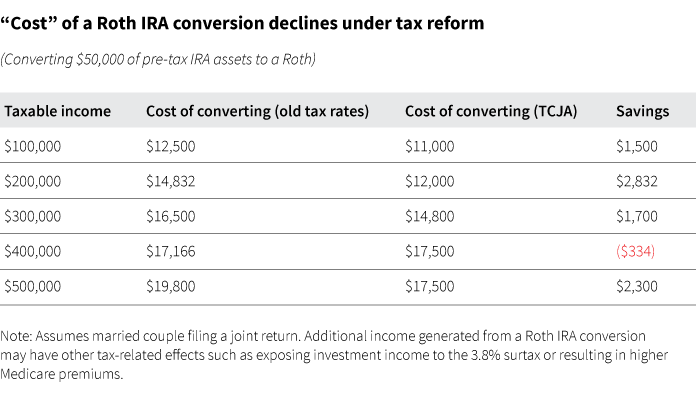

Reduced taxes means lower costs

For many taxpayers, the “cost” of a Roth IRA conversion has declined. Consider some examples of a taxpayer converting $50,000 of traditional IRA assets under the new tax regime. At most levels, the cost of converting would be lowered, although at the $400,000 level, taxpayers would owe slightly more.

Planning considerations

Prior to tax reform, it generally made sense for taxpayers to convert IRA assets early in the year to maximize the amount of time before the tax filing deadline and to determine whether to undo the conversion. Also, with the option to recharacterize the entire conversion or a portion, IRA owners were able to “guesstimate” how much to convert without being fully committed to that amount.

With the implementation of tax reform, it may make sense to wait until the end of the calendar year. This provides more time for taxpayers to fully understand what their taxable income will look like and the consequences of adding more income from a Roth IRA conversion.

Lastly, certain taxpayers in the 24% tax bracket may find a partial Roth IRA conversion makes sense. For married couples, the new 24% bracket ($165,000 to $315,000 in taxable income) is significantly lower than the previous system where taxpayers would have paid either 28% or 33% on that income.

The decision to convert is complex, depending on the potential for overall tax rates to increase (or decrease) in the future, and a taxpayer’s likely tax bracket in retirement and ability to pay the conversion tax with non-retirement funds. With any tax planning strategy, it is important to discuss the impact of an IRA conversion on your overall financial plan with a qualified tax professional.

312552

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.