The recently passed SECURE Act provides for many changes to retirement accounts as well as some tax-related items.

One change impacts the “kiddie tax,” which applies to the unearned income of minors generated within custodial UTMA or UGMA accounts. Unearned income above a certain threshold – $2,200 for 2019 (and 2020) – is subject to the kiddie tax. The tax was designed to prevent families from holding investments in the name of a minor to avoid or limit taxation.

Until 2018, the kiddie tax applied the parent’s marginal tax rate to unearned income above the threshold. The passage of the Tax Cuts and Jobs Act (TCJA) made changes to base the kiddie tax on the same tax schedule that applies to trusts and estates.

For 2020 and forward, the new law reverts the kiddie tax back to the previous method of applying the parent’s marginal tax rate.

Taxpayers have the option of applying either method – the tax rate associated with trusts and estates, or the parent’s marginal tax rate for tax years 2018 and 2019. A taxpayer wishing to change the method for 2018 would have to file an amended tax return. For taxpayers holding custodial accounts and filing 2019 taxes in the next few months, a key decision will be which method to use.

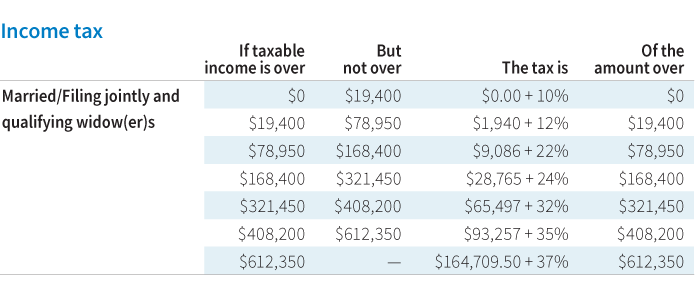

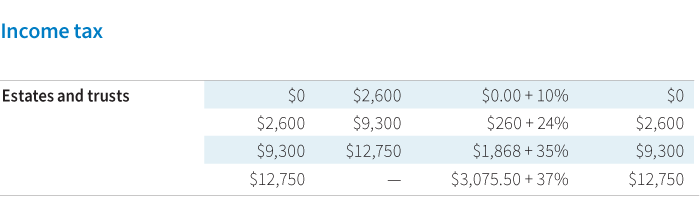

For tax year 2019, here’s a comparison of the trust/estate tax rate schedule vs. married filing jointly tax schedule:

When comparing the two tax calculation options for 2019, here are some considerations:

- Parents subject to the highest marginal tax rate already, or have lower amounts of unearned income subject to the kiddie tax, may find the trust and estate tax schedule more beneficial

- Parents in a lower-to-moderate tax bracket with larger amounts of unearned income subject to the kiddie tax may find that using their own marginal tax bracket (vs. the tax brackets for trusts and estates) may be more beneficial

- Given the complexity around the kiddie tax calculation, it is critical to work with a tax professional who can calculate each scenario to determine the best option

Planning considerations for tax mitigation

Depending on the amount of unearned income, parents may want to consult a financial advisor for strategies to mitigate the tax impact. For example, parents may want to change the underlying investments and select others that may not generate as much income or dividends subject to the tax.

If the funds are being saved for education, parents may consider transferring the account to a 529 college savings plan, where earnings grow tax free. Also distributions for qualified education expenses would not be subject to taxation. There are specific rules applied to assets in a 529 plan that originated from a custodial account, so it’s critical to consult with a financial advisor or tax professional.

320135

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.